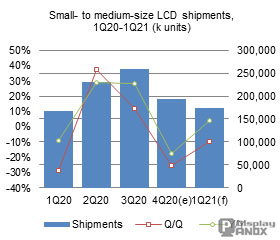

Taiwan's shipments of small to medium-sized LCD panels are projected to reach 174 million units in the first quarter of 2021, representing a 9.5% sequential decline, despite a 3.9% year-over-year increase. While the annual growth signals some resilience, underlying market dynamics and supply constraints point to structural challenges ahead.

Q1 Decline Driven by Component Shortages and Holiday Downtime

The anticipated quarterly decline is largely due to shortages of critical components, particularly LCD driver ICs, which have tightened supply chains and disrupted production schedules. Additionally, the reduced number of working days during the Lunar New Year holiday further limited output across the industry.

Q2 22020 Recap: Shipments Slump Amid Sanctions and Strategic Shifts

In the fourth quarter of 2020, Taiwan’s small to mid-size LCD panel shipments dropped to 193 million units, down 25.3% quarter-over-quarter and 17.8% year-over-year. This decline was driven by two major factors:

Tightened U.S. trade sanctions on Huawei, which forced downstream clients to cut or delay orders;

A strategic shift by panel makers toward notebook and large tablet panels (over 10.1 inches) to meet booming demand for remote work and distance learning devices.

Application Segment Trends: Handset Demand Slows, Tablet and Automotive Recover

Smartphone panel shipments saw a significant decline in Q4, largely due to seasonal demand slowdowns and front-loaded orders in Q3. In contrast, tablet panel shipments gained momentum, supported by demand from major clients such as Amazon, which saw increased sales in the budget and mid-range tablet segments.

Meanwhile, automotive panel shipments rebounded, driven by the gradual recovery of the global automotive industry, prompting panel makers to shift focus toward this growing application sector.

2021 Outlook: Full-Year Shipments to Decline 6.8% as AMOLED Gains Ground

Meanwhile, automotive panel shipments rebounded, driven by the gradual recovery of the global automotive industry, prompting panel makers to shift focus toward this growing application sector.

2021 Outlook: Full-Year Shipments to Decline 6.8% as AMOLED Gains Ground

Looking ahead, Taiwan's total shipments of small to mid-size LCD panels in 2021 are forecast to decline 6.8% year-over-year to 790 million units. The primary factor behind this projected decline is the continued rise of AMOLED panels in the smartphone segment, which are steadily eroding LCD’s market share due to their superior contrast, lower power consumption, and flexibility.

With more smartphone brands adopting AMOLED as a standard for mid-to-high-end models, the structural shift in display technologies is expected to accelerate throughout the year.

Strategic Outlook: Diversification Key to Sustaining Growth

With more smartphone brands adopting AMOLED as a standard for mid-to-high-end models, the structural shift in display technologies is expected to accelerate throughout the year.

Strategic Outlook: Diversification Key to Sustaining Growth

Facing intensifying competition and technological transitions, Taiwan’s panel makers must diversify into emerging application areas such as automotive displays, industrial control panels, and wearable devices. Strengthening supply chain resilience and focusing on product differentiation will be critical for maintaining competitiveness in the evolving global panel market.